Public health insurance Germany 2026: what changed and how to pick a Krankenkasse

What changed in German public health insurance for 2026: average Zusatzbeitrag is now 2.9 percent, income ceiling moved up, and how to compare Kassen.

Table of contents

Last updated: June 2026

TL;DR: From January 2026 the average public-health-insurance Zusatzbeitrag rose from 2.5% to about 2.9%, lifting the total contribution to roughly 17.5% of gross pay. The Beitragsbemessungsgrenze (income ceiling) climbed to €5,812.50 a month (€69,750 a year). TK and AOK Bayern are still the cheapest big-name picks at 2.69%. BARMER stayed at 3.29%, DAK jumped from 2.80% to 3.20%. If your Kasse raised its rate, you have a Sonderkündigungsrecht and can switch on one month's notice.

Public health insurance (Gesetzliche Krankenversicherung, GKV) is the system most people in Germany are on, including the vast majority of international students, employees, and dependents. It costs more in 2026 than it did in 2025, and the gap between the cheapest and most expensive Kassen has widened. This post walks through the actual numbers, what changed on 1 January 2026, and how to pick or switch a Krankenkasse without overpaying.

For the high-level overview of how German healthcare works, including private insurance and the Gesundheitskarte, start with our health insurance pillar. For a short primer on every insurance type a new arrival actually needs, see our companion piece on must-have insurance in Germany.

What changed in public health insurance for 2026

Three numbers moved on 1 January 2026, and one stayed the same:

- Average Zusatzbeitrag rose from 2.5% to roughly 2.9%. The federal cabinet announced the new average in November 2025, and individual Kassen published their 2026 rates over the following weeks. Most major Kassen raised their rate, several by more than the average.

- Beitragsbemessungsgrenze rose from €5,512.50 to €5,812.50 a month (from €66,150 to €69,750 a year). This is the income ceiling above which contributions stop accruing. Anyone earning above the old ceiling now pays GKV on €300 more per month.

- Pflegeversicherung (long-term care) held the same rates that took effect in mid-2025: 3.6% for parents with at least one child, 4.2% for childless members aged 23 and older, with extra reductions for parents of multiple children under 25.

- The base rate (14.6%) is unchanged. It is set by federal law and is identical at every statutory Kasse. The only fund-specific lever is the Zusatzbeitrag.

The combined effect: an employee on the new ceiling of €5,812.50 a month at a 2.9% Zusatzbeitrag pays about €510 a month in employee-share GKV contributions plus around €245 in Pflegeversicherung if they are childless and over 23. Total monthly deductions on health and long-term care alone reach roughly €755. The employer pays a matching share of the GKV contribution.

How GKV is calculated in 2026

GKV has a clean formula. Three components, applied to gross income up to the ceiling:

| Component | 2026 rate | Who pays |

|---|---|---|

| Allgemeiner Beitragssatz (general rate) | 14.6% | Split 50/50 employer/employee |

| Zusatzbeitrag (per Kasse) | 2.18% to 4.39% | Split 50/50 employer/employee |

| Pflegeversicherung | 3.6% (parents) or 4.2% (childless 23+) | Split 50/50 employer/employee, plus a 0.6% childless surcharge entirely on the employee |

Multiply the combined rate by your monthly gross pay (capped at €5,812.50). For self-employed members in voluntary GKV the same percentages apply, but the member pays the full amount, not just half.

Worked example, employed, €60,000 gross a year (€5,000 a month):

- 14.6% × €5,000 = €730 (split, so €365 employee share)

- 2.9% × €5,000 = €145 (split, so €72.50 employee share)

- 4.2% × €5,000 = €210 (split as 3.6% + 0.6%, so €120 employee share)

- Employee-side total: about €557.50 a month, or 11.15% of gross.

Worked example, employed, €72,000 gross a year (€6,000 a month, above the ceiling):

- The contribution is calculated on €5,812.50, not €6,000. Anything above the ceiling is contribution-free.

- Employee-side total at TK's 2.69% Zusatzbeitrag: about €633 a month.

Worked example, self-employed in voluntary GKV:

- Same percentages, but you pay the full amount. On the new minimum assessment basis of €1,248.33 a month for 2026, you pay roughly €260 to €290 depending on your Kasse.

- Above the ceiling, contributions cap at the same €5,812.50 base. The maximum monthly cost works out to roughly €1,260 in 2026 for a childless member at an average Kasse.

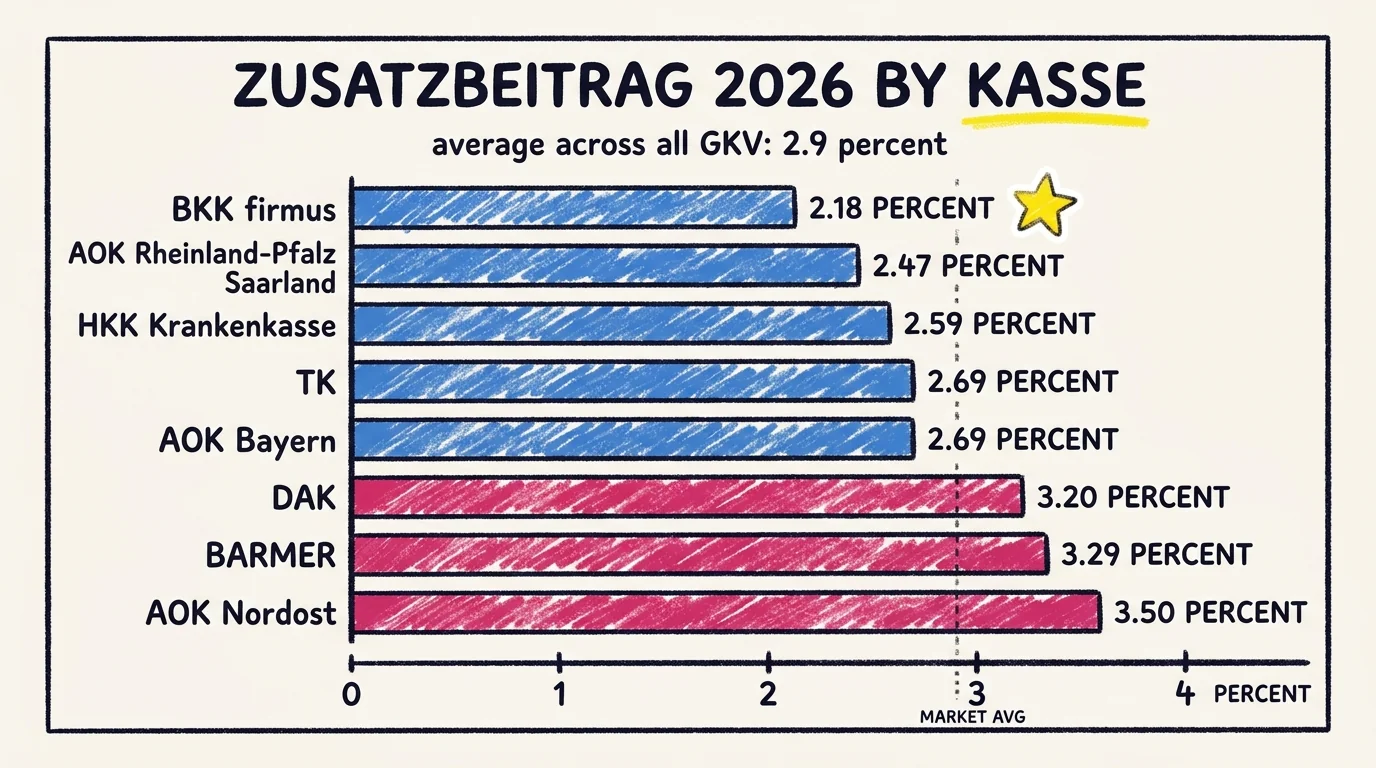

TK vs AOK vs DAK vs BARMER: the 2026 Zusatzbeitrag comparison

Below is the 2026 Zusatzbeitrag for the eight Kassen most expat readers ask about. The base rate (14.6%) and Pflegeversicherung are identical everywhere, so the Zusatzbeitrag is the only number that moves your bill.

| Kasse | 2026 Zusatzbeitrag | Change from 2025 | Why people pick it |

|---|---|---|---|

| BKK firmus | 2.18% | unchanged | Cheapest open Kasse nationwide |

| AOK Rheinland-Pfalz/Saarland | 2.47% | unchanged | Cheapest big-brand AOK region |

| HKK Krankenkasse | 2.59% | up from 2.19% | Low rate, no English service |

| TK (Techniker Krankenkasse) | 2.69% | up from 2.45% | Best English support, big-name brand |

| AOK Bayern | 2.69% | unchanged | Tied for cheapest big AOK, large branch network |

| DAK-Gesundheit | 3.20% | up from 2.80% | Strong alternative-medicine extras |

| BARMER | 3.29% | unchanged | Strong telemedicine and mental-health extras |

| AOK Nordost (Berlin, Brandenburg, MV) | 3.50% | unchanged | Most expensive of the open big-brand options |

The full statutory list runs from 2.18% up to 4.39%. The market average is about 2.9%. Anything below 2.5% is genuinely cheap. Anything above 3.5% is meaningfully expensive once you compound it across a year of salary.

For a typical employee earning €5,000 a month, the difference between a 2.5% and a 3.5% Zusatzbeitrag is €50 a month gross, or €25 a month after the employer's half is deducted. Over a full year that is €300 of net pay, on identical legal benefits.

The four most-asked-about Kassen on a side-by-side view:

| Feature | TK | AOK Bayern | BARMER | DAK |

|---|---|---|---|---|

| 2026 Zusatzbeitrag | 2.69% | 2.69% | 3.29% | 3.20% |

| Member count | 12.3M | ~5M (Bayern only; AOK group total: 27M) | 8.2M | 5.6M |

| English support | 24/7 hotline, English app, English website | Limited, varies by branch | Weekday English hotline, English student page | Very limited |

| Branch network | About 200 | 1,400+ across the AOK group | About 400 | About 800 |

| Telemedicine | TK-Doc video | Regional partners | Teledoktor app | DAK app, basic |

| Headline extras | Cash bonus up to €200 a year | Local doctor partnerships | 7Mind app free 12 months, online CBT | Uncapped point-based cash bonus, alternative-medicine subsidies |

The legally mandated benefits are the same at every Kasse: hospital stays, doctor visits, prescriptions, dental checkups, mental-health care, maternity, vaccinations. What differs is the service quality, the digital tools, and the bonus programs.

Which Krankenkasse is right for you

There is no single best Kasse. The right pick depends on your German level, where you live, and what extras matter to you. A short decision guide:

- You just arrived, your German is weak, and you want everything in English: TK. The 24/7 English hotline, English app, and English member portal are unmatched among the big four.

- You live in Bavaria and want the cheapest big-name option: TK or AOK Bayern, both at 2.69%.

- You live in Rheinland-Pfalz or Saarland: AOK Rheinland-Pfalz/Saarland at 2.47% is the cheapest mainstream pick.

- You speak B1+ German and want the absolute cheapest open Kasse: BKK firmus at 2.18%, or HKK at 2.59%. Service is German-only.

- Mental health support matters to you (anxiety, exam stress, therapy access): BARMER. The free 12-month 7Mind subscription, online CBT, and Teledoktor are real differentiators.

- You travel home often and want full vaccination cover: BARMER reimburses 100% of travel vaccinations.

- You use alternative medicine (osteopathy, acupuncture, homeopathy): DAK. The strongest set of subsidies among the big four.

- You like walk-in branches in small towns: AOK. The 1,400+ offices across the regional AOK federation are the densest physical network of any Kasse.

- Your Kasse just raised its Zusatzbeitrag and you want to leave: every member with a rate hike has a Sonderkündigungsrecht, see the next section.

If your situation is genuinely budget-first and English support is not critical, BKK firmus is roughly €600 a year cheaper than BARMER on a €60,000 salary. If English support is critical, TK is the only big-four Kasse with a fully English service stack.

How to switch your Krankenkasse

Switching is simpler than most people expect. The rules:

- Bindungsfrist: when you join a new Kasse you commit to staying 12 months before you can switch again. This is a federal rule, not a Kasse-level one.

- Notice period: to leave a Kasse you give two months' notice to the end of a month. Notice given on 15 January ends membership on 31 March.

- Sonderkündigungsrecht (special right): if your Kasse raises its Zusatzbeitrag, you get one month's notice to leave, regardless of the 12-month lock. The deadline is the end of the month before the new rate kicks in. If your Kasse raised rates effective 1 January 2026, the cancellation window ran through January.

- Paperwork loop is automatic: to switch, you sign up at the new Kasse and they cancel the old one for you. You do not need to write to the outgoing Kasse yourself.

A typical switch takes one to four weeks of administrative time. Your old insurance card stays valid until the switch date. The new Kasse issues a fresh elektronische Gesundheitskarte (eGK) within two weeks. Pending claims and ongoing prescriptions transfer automatically. Existing primary doctor and specialist relationships continue without disruption.

If you are not sure whether your Kasse raised its rate, log in to the member portal or open the most recent Beitragsbescheid. Any rate change must be communicated in writing at least one month before it takes effect, and the letter is required by law to mention the Sonderkündigungsrecht explicitly.

Special cases

Students under 30 (KVdS)

International and domestic students under 30, enrolled in a degree program, pay a fixed rate set by federal law. The base premium is €87.38 a month at every Kasse, plus the Kasse's own Zusatzbeitrag share, plus Pflegeversicherung. For 2026:

- TK or AOK Bayern (under 23 or with at least one child): €141.16 a month (€87.38 base + €23.00 Zusatzbeitrag at 2.69% + €30.78 Pflege at 3.6%).

- TK or AOK Bayern (23+ childless): €146.29 a month (€87.38 + €23.00 + €35.91 Pflege at 4.2%).

- BARMER (23+ childless): €151.42 a month.

- DAK (23+ childless): €150.65 a month.

Language-course students and Studienkolleg students are not covered by KVdS and need private incoming insurance instead. The base €87.38 figure applies only to enrolled degree students under 30.

Working professionals at the contribution ceiling

Employees on €5,812.50 a month or more pay the maximum GKV contribution. At an average Zusatzbeitrag of 2.9% and the 4.2% Pflege rate, this works out to roughly €755 a month total cost (employer plus employee combined). The employee share is around €380 plus the 0.6% childless surcharge of about €17, so roughly €397 net out of pocket. Earning more than the ceiling does not raise the contribution.

Self-employed and freelancers in voluntary GKV

Self-employed members in voluntary statutory insurance pay the full contribution themselves, with no employer share. The 2026 minimum assessment base is €1,248.33 a month. Expect monthly contributions between €255 and €295 at the floor, and up to about €1,260 at the ceiling. Many freelancers compare voluntary GKV against private insurance (PKV) once their income passes the Versicherungspflichtgrenze, currently €77,400 a year. Switching back from PKV to GKV is hard after age 55, so the decision is more permanent than it first looks.

Family insurance (Familienversicherung)

Spouses and dependent children can be insured for free under a working member's GKV policy if the dependent's monthly income is below €556. This is one of the most underused benefits of GKV, and it remains intact in 2026. There is no extra paperwork beyond the initial Familienversicherung application.

Common mistakes to avoid

- Picking on Zusatzbeitrag alone. A 0.1% gap is about €5 a month on a €5,000 salary, half of that after the employer share. If switching kills your English support or moves you to a Kasse with no nearby branches, the saving is rarely worth it.

- Missing the Sonderkündigungsrecht window. When your Kasse announces a rate hike, the special cancellation right has a fixed deadline. Once it passes you are back on the 12-month lock.

- Confusing the Zusatzbeitrag with the Pflege rate. Pflegeversicherung is set by federal law and identical at every Kasse. Only the Zusatzbeitrag varies.

- Auto-rolling into the regional AOK without comparing. New arrivals are often steered to "their" regional AOK at the Bürgeramt or by an employer's HR. Some regional AOKs (Nordost at 3.50%, Rheinland/Hamburg and Bremen at 3.29%) are noticeably more expensive than TK or AOK Bayern.

- Forgetting the legally fixed parts are equal everywhere. The 14.6% base rate, the €87.38 student premium, and the Pflege rates are federally set. No Kasse can legally undercut them.

- Treating GKV bundled blocked-account packages as locked-in. Student insurance bundled with services like Fintiba or Expatrio often defaults to TK, but you can switch any statutory Kasse later. The blocked account itself is independent of the GKV pick.

FAQ

Is TK still the cheapest public health insurer in Germany for 2026?

Among nationwide big-name Kassen, TK at 2.69% is tied with AOK Bayern as the cheapest. The absolute cheapest open Kasse in 2026 is BKK firmus at 2.18%. AOK Rheinland-Pfalz/Saarland at 2.47% is the cheapest big-brand AOK region. TK still wins on English-language service, which is why most international arrivals pick it.

What does the Zusatzbeitrag hike actually cost me on a €60,000 salary?

The average Zusatzbeitrag rose from 2.5% to 2.9%. On €5,000 a month gross, that is €20 a month more in total contribution, or €10 a month after the employer's half. Annualised, the average employee earning €60,000 a year pays about €120 more in 2026 than in 2025, before counting the higher contribution ceiling.

Can I switch from TK to BARMER mid-year if I just joined?

The 12-month Bindungsfrist applies. If TK raised its Zusatzbeitrag during your membership (which it did for 2026, from 2.45% to 2.69%), you have a Sonderkündigungsrecht and can switch with one month's notice regardless of the lock. Outside that window, you wait until the 12 months are up, then give two months' notice.

What is the Beitragsbemessungsgrenze and why does it matter?

It is the gross-income ceiling above which GKV contributions stop accruing. For 2026 it is €5,812.50 a month, up from €5,512.50. If you earn above the ceiling, your contribution is calculated on €5,812.50, not your full salary. The €300-a-month ceiling rise costs high earners about €60 a month in extra GKV contribution before the employer share.

Do students pay the same as employees?

No. Students under 30 in a degree program pay the fixed Krankenversicherung der Studenten (KVdS) rate: €87.38 a month base, plus the Kasse's Zusatzbeitrag share on a €855 calculation base, plus Pflege. The total is €141.16 to €151.42 a month depending on the Kasse, age, and whether you have children. Employed students above the working-student threshold (over 20 hours a week during term) shift to regular GKV with employer-shared contributions.

Will my Pflegeversicherung also rise in 2026?

The Pflege rate is unchanged in 2026: 3.6% for parents, 4.2% for childless members aged 23 and older. The Bundestag debated a further increase in late 2025 but did not pass one for the 2026 cycle. Expect a reassessment in 2027.

Can I keep private insurance instead of GKV?

If you are employed and earn above the Versicherungspflichtgrenze (€77,400 a year for 2026), you can opt out of GKV and into private insurance (PKV). Self-employed members and civil servants can choose freely. PKV often looks cheaper at age 30 and considerably more expensive at age 60. Switching back to GKV after age 55 is restricted by federal rules.

How long does switching Kassen actually take?

Typically one to four weeks. You sign up at the new Kasse, they handle the cancellation paperwork with your old Kasse, and you receive a fresh Gesundheitskarte within two weeks. Existing prescriptions, primary-doctor relationships, and pending claims transfer automatically. You do not need to inform your employer until the switch takes effect, after which payroll updates the Kasse on file.

Where to next

- Health insurance pillar for the full picture, including private insurance and add-ons.

- Must-have insurance in Germany for liability, household contents, and other policies most expats actually need.

- Healthcare system guide for international students for how the Gesundheitskarte, Hausarzt, and referrals work.

- Cost calculator for a full monthly budget that includes GKV.

Continue reading

Living in Germany·19 min read

Public vs Private Health Insurance in Germany: PKV vs GKV Head-to-Head with Real Numbers

Public vs private health insurance in Germany compared with 2026 numbers. JAEG, BBG, GKV monthly cost, PKV premiums, family math, and the age 55 lock-in.

Read articleLiving in Germany·15 min read

Rundfunkbeitrag explained: why every German household pays it and how students legally skip it

Germany's broadcasting fee in 2026: who pays, who is exempt, how to apply for the Befreiung, and what happens if you ignore the bill.

Read articleLiving in Germany·16 min read

Anmeldung in Germany 2026: How to actually get a Bürgeramt appointment in Berlin, Munich, Hamburg

Anmeldung in Germany 2026: how to actually get a Bürgeramt appointment in Berlin, Munich and Hamburg. Wait times, documents, fines, online route.

Read articleReady to plan your Germany journey?

Explore our tools and resources to find the perfect university and program for your academic goals.