Best German bank accounts for expats in 2026

Compare the eight most popular German bank accounts for expats in 2026. Real fees, ATM rules, English support, and a clear pick for first arrivals.

Table of contents

Last updated: May 2026

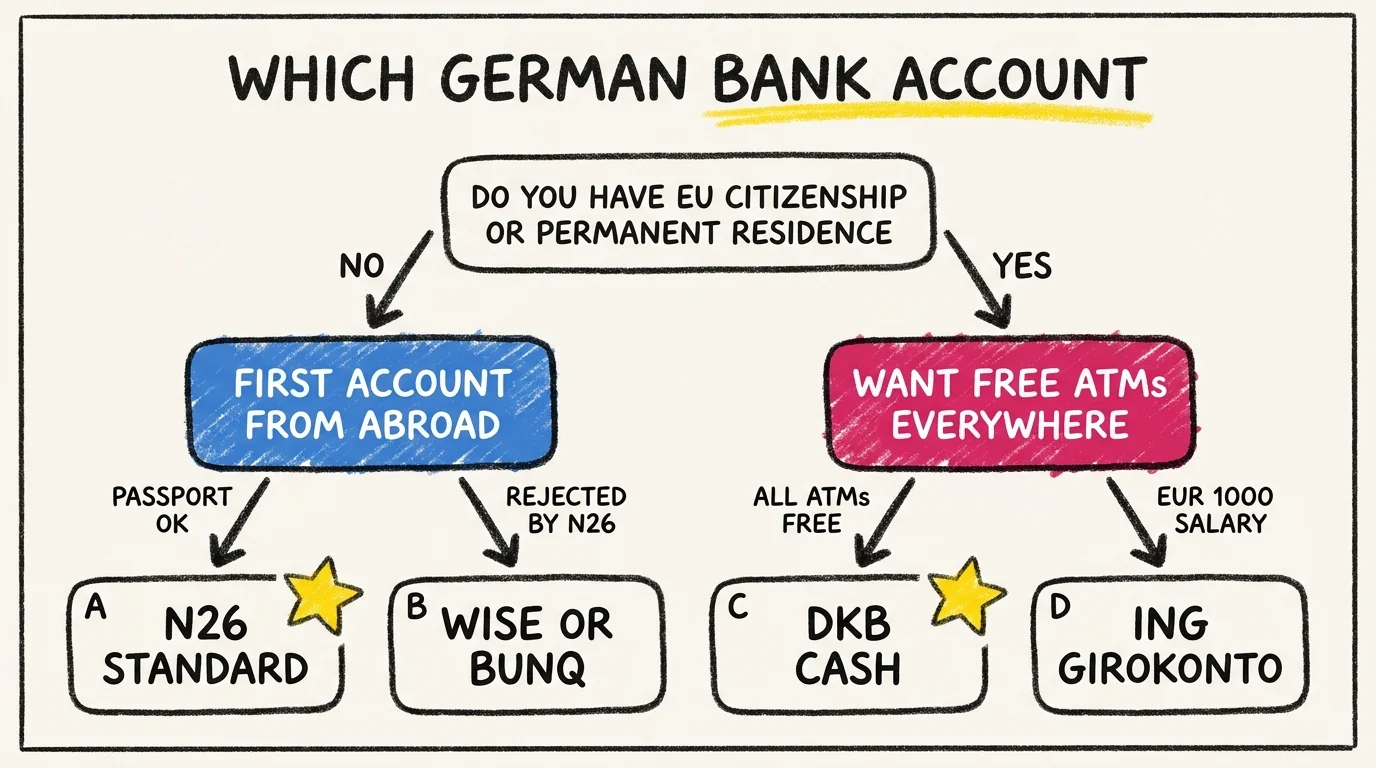

TL;DR: For most expats arriving in Germany in 2026, N26 Standard is the easiest first bank account: free, English-friendly, German IBAN, no Anmeldung needed. Pair it with Wise for cross-border salary or family transfers. Pick DKB or ING later, after you have permanent residence and want a richer feature set. Avoid Revolut as your first account since it requires a German tax ID, which you only get after Anmeldung.

You moved to Germany. Your landlord wants the deposit by IBAN, your employer needs salary details on day one, and every bank seems to want a document you do not have yet.

This guide compares the eight bank accounts expats actually look at in 2026, lines up real 2026 fees and requirements, and tells you which to open first. For the broader money setup, read the finances pillar guide. For the student case, see opening a German bank account for international students.

Which German bank account is best for expats in 2026?

The single best first account for most expats is N26 Standard: free, opens in minutes from your phone, German IBAN, full English support, no Anmeldung required, no minimum deposit. It covers rent transfers, salary deposits, the Deutschland-Ticket, and tax-office direct debits without a monthly fee. It also creates your first Schufa record, which helps when you apply for an apartment.

The catch: N26 only accepts certain passport types and may ask for a plastic residence permit valid 12 months. If you fail their identity check, bunq and Wise accept more nationalities. If you already have permanent residence or EU citizenship, DKB and ING beat N26 on free ATMs and feature depth. Revolut works fine as a second account but cannot be your first because you need a tax ID to open it.

What "expat-friendly" actually means in 2026

An expat-friendly bank in 2026 should:

- Open the account remotely, from your phone, ideally before you arrive

- Accept your passport without demanding a 12-month residence permit on day one

- Issue a German IBAN starting with

DE, since some German employers and landlords still reject foreign IBANs even though that is illegal under EU law - Speak English in customer service, online banking, and contracts

- Charge no monthly fee on the basic tier

- Refund or waive ATM fees on the standard German networks

- Create a Schufa record, since you will need one to rent an apartment

The eight banks below clear most of these bars. None clear all of them.

The shortlist: eight bank accounts worth comparing

We narrowed the field to these eight based on which accounts new arrivals open most often, which actually accept non-EU expats, and which have current 2026 pricing pages.

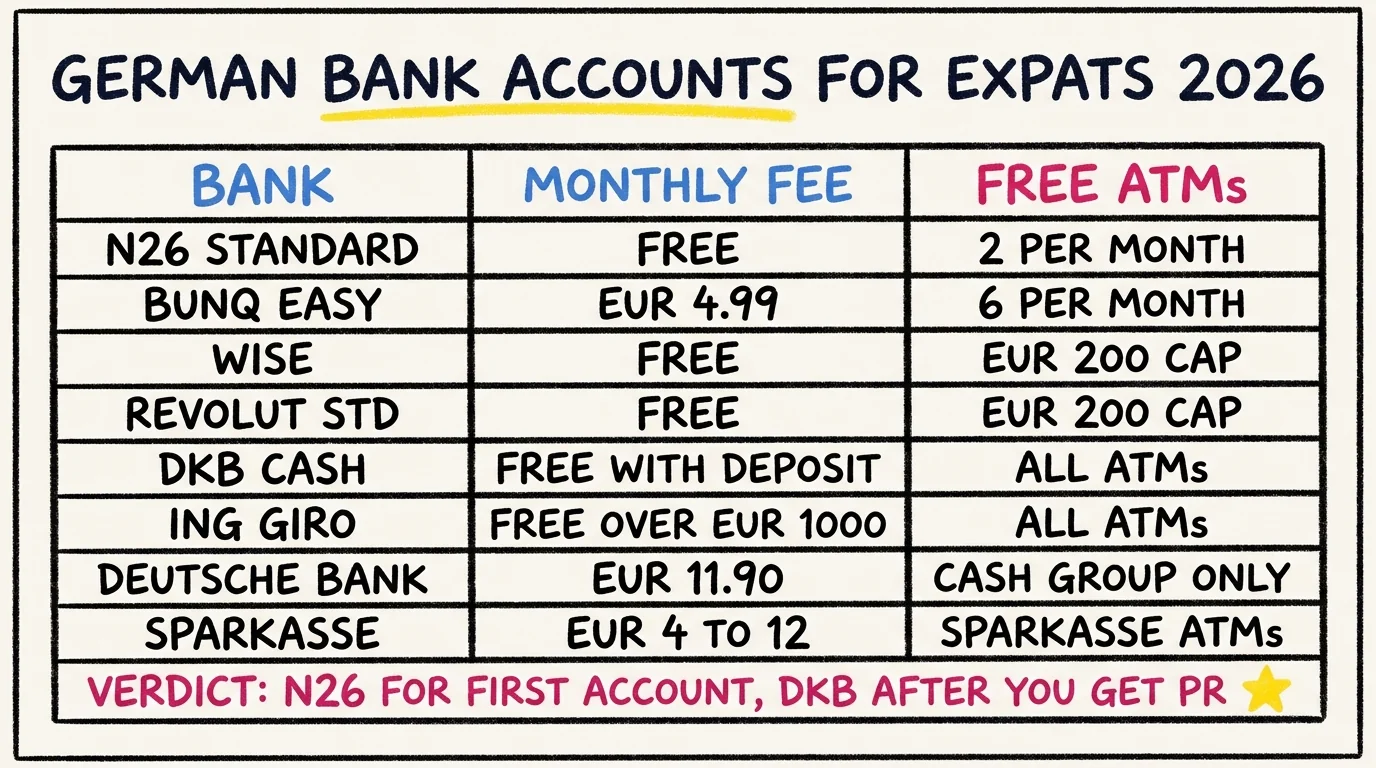

| Bank | Type | Monthly fee | Free ATMs | German IBAN | Opens before Anmeldung | English |

|---|---|---|---|---|---|---|

| N26 Standard | Digital | Free | 2 per month, then EUR 2 each | Yes | Yes | Yes |

| bunq Easy Bank | Digital | EUR 4.99 | 6 per month | Yes | Yes | Yes |

| Wise | Digital, multi-currency | Free | EUR 200 per month free | No, Belgian IBAN | Yes | Yes |

| Revolut Standard | Digital | Free | EUR 200 per month free | Lithuanian IBAN by default, German on Premium | No, needs tax ID first | Yes |

| DKB Cash | Direct bank | Free with monthly deposit | All German ATMs free | Yes | Yes, but EU citizenship or PR required | German only |

| ING Girokonto | Direct bank | Free with EUR 1,000 monthly deposit | All German ATMs free, EUR 50 minimum | Yes | No, Anmeldung required | German only |

| Deutsche Bank Konto | Traditional | EUR 11.90 standard, free for EU students under 30 | Cash Group ATMs free, others EUR 6 | Yes | Yes, but slow process | Online banking and customer service in English |

| Sparkasse Giro | Traditional with branches | EUR 4 to EUR 12 depending on Land | Sparkasse ATMs free, others ~7.50 | Yes | No | Online banking only |

Two banks worth a quick mention but not in the main table: C24 (the only free German account with a Girocard, but German-only and rejects many passports) and Tomorrow / Vivid (sustainability and crypto angles, both fine, but neither is materially better than N26 for the typical expat).

Digital-first banks: which one and why

N26

The default first account. Free Standard tier, German IBAN, app-only, opens in 8 minutes. Two free ATM withdrawals a month, then EUR 2 per withdrawal. Pays the EUR 100,000 EU deposit guarantee. Speaks English, French, German, Italian, Spanish.

Paid tiers exist if you withdraw cash often: N26 Smart at EUR 4.90 per month adds 5 free withdrawals, N26 Go at EUR 9.90 adds insurance, N26 Metal at EUR 16.90 is mostly cosmetic. Most expats stay on Standard for years.

The risk: N26's identity check rejects some passports. If you are Russian, Iranian, or hold a passport on their excluded list, do not waste a day applying. Go straight to bunq, Wise, or Sparkasse.

Wise

Best as a second account, sometimes as a first. Free to open, no monthly fee, works in 40 currencies. The catch: your German IBAN is not actually German. Wise gives you a Belgian or other EU IBAN, which is legal everywhere in the SEPA zone but occasionally rejected by lazy German employers and landlords.

Use Wise when: you need to receive salary in multiple currencies, send money home cheaply, or open an account before you arrive in Germany. The mid-market exchange rates beat every traditional bank's transfer fee.

Revolut

A solid second account, never a first. Revolut requires a German tax ID to open the account. You only get a German tax ID after Anmeldung, and you can only do Anmeldung after you find an apartment, which usually takes a German bank account first. The chicken-and-egg traps recent arrivals every month. Open N26 or Wise first, then add Revolut once you have your tax ID.

Once active, Revolut Standard is free and gives you EUR 200 per month in free ATM withdrawals. Premium tiers add a German IBAN and travel insurance.

bunq

The best fallback when N26 rejects your passport. EUR 4.99 per month for the Easy Bank tier, German IBAN, six free ATM withdrawals a month, accepts more nationalities. No Schufa record gets created, which is mostly bad (you want a Schufa for apartments) but occasionally good (if your home country credit history is weak).

Traditional and direct banks: when to switch

DKB Cash

The expat favourite once you qualify. Free with a regular monthly deposit, German IBAN, free withdrawals at every German ATM, free credit card on the standard tier. The blocker for new arrivals: DKB requires EU citizenship or German permanent residence. If you have neither, your application gets rejected. Switch to DKB after 21 to 33 months in Germany once your residence permit converts to a Niederlassungserlaubnis.

ING Girokonto

Same story as DKB. Free if you deposit EUR 1,000 a month, free ATM withdrawals (EUR 50 minimum), strong app, but you need EU citizenship or permanent residence to open it. Their student tier is slightly more lenient and waives the deposit requirement under 28 years old.

Deutsche Bank Konto

Slow to open. Two to four weeks of paperwork, document checks, and a branch visit. Worth it if you want a major bank with English-speaking staff, branches across Germany, and a credit card you can actually use abroad. The Young account is free for EU students under 30. The standard account costs EUR 11.90 per month, which most expats will not justify against a free N26 Standard.

Sparkasse Giro

The bank for everything else: people from sanctioned countries (Russia, Iran, Syria, others) who get rejected by the digital banks, anyone who genuinely needs a branch, anyone whose employer or landlord insists on a "real" German bank. Pricing varies by Bundesland; expect EUR 4 to EUR 12 a month. Sparkasse ATMs cover roughly 45 percent of the country, so you almost never pay an ATM fee.

Sparkasse also offers Sperrkonto (blocked account) at some branches, though most students use Expatrio since Fintiba was acquired by Expatrio in 2025.

How to pick the right one in five questions

- Are you already in Germany with an Anmeldung and tax ID? If no, start with N26 or Wise.

- Do you have EU citizenship or Niederlassungserlaubnis? If yes, DKB or ING beats every digital bank on free ATMs and features.

- Will your employer accept a non-DE IBAN? Most do; some still do not. If unsure, pick a bank with a German IBAN.

- Do you need physical branches? Sparkasse and Deutsche Bank are the only realistic options.

- How often do you need cash? If more than four ATM trips a month, avoid N26 Standard's two-free limit. Go to DKB, bunq paid, or Sparkasse.

If your answers point to "first arrival, non-EU passport, want everything in English, no plans to use a branch," the answer is N26 Standard, then add Wise for cross-border money. That covers 80 percent of new expats.

Documents you actually need to open an account

For a digital bank (N26, bunq, Wise, Revolut after tax ID):

- Valid passport

- A Germany-registered phone number

- A residential address (Anmeldung not always required, but a real address is)

- Proof of income or employment if applying for a credit card

For a traditional bank (DKB, ING, Deutsche Bank, Sparkasse):

- Valid passport plus residence permit (Aufenthaltstitel)

- Anmeldung certificate (Wohnungsgeberbestaetigung plus Anmeldebestaetigung)

- Tax ID (Steueridentifikationsnummer)

- Proof of income (last three payslips or work contract)

The biggest practical block for expats is the order: many banks demand Anmeldung, but Anmeldung is easier with proof of a German bank account. The standard fix is to open N26 or Wise first, do Anmeldung, then add a traditional bank later.

Common mistakes when picking a German bank

- Opening Revolut as your first account. It requires a tax ID. New arrivals lose a week realising this.

- Paying for a Deutsche Bank or Sparkasse account when N26 is free. Unless you genuinely need a branch, the EUR 100 a year is wasted money.

- Treating "free Girocard" as a deal-breaker. Girocards matter for some German shops that reject Visa, but the share is dropping fast in 2026. Berlin and Munich shops mostly accept Mastercard and Visa now.

- Ignoring the Schufa angle. Your bank account is one of the easiest ways to start a Schufa record, which you need to rent an apartment. Wise and bunq do not create one. N26 does.

- Skipping deposit insurance. Every bank in this guide is covered by EU or German deposit guarantee schemes up to EUR 100,000 per customer per bank. Confirm this before depositing more.

Frequently asked questions

Can I open a German bank account before I arrive in Germany?

Yes, with Wise, N26 (in some cases), and bunq. Wise is the most flexible since it does not need a German address. N26 prefers a German address but accepts some EU addresses temporarily. Traditional banks like DKB and Deutsche Bank generally require you to be in Germany.

Do I need a German bank account if I already have an EU bank account?

Legally no. EU IBAN discrimination is illegal and any euro account in the SEPA zone works for German salary, tax, and rent. Practically, some German employers, landlords, and government offices still create friction with non-DE IBANs. A German IBAN saves you arguments.

Is N26 really a "real" German bank?

Yes. N26 holds a full German banking licence from BaFin, your deposits are protected up to EUR 100,000 by the EU Deposit Guarantee Scheme, and it issues German IBANs. The "neobank" label is about app-first design, not legal status.

Which bank is best for receiving my salary?

Any bank with a German IBAN. N26, DKB, ING, Deutsche Bank, Sparkasse, and bunq all work. Wise can receive salary too but in EUR, since the German IBAN matter is mostly about edge-case payment portals, not payroll.

Which bank is best if I get rejected by N26?

bunq accepts more passport types, especially non-EU and post-Soviet citizens. Wise accepts almost everyone. Sparkasse takes citizens of sanctioned countries that digital banks reject. Try in that order.

What is the cheapest way to send money from Germany to my home country?

Wise for most corridors. Traditional bank wires (Deutsche Bank, Sparkasse) cost EUR 15 to EUR 25 per transfer plus a 2 to 4 percent exchange rate margin. Wise charges roughly 0.5 to 1 percent at the mid-market rate. The savings on a single rent-month transfer pay for a year of N26 Standard.

Where to next

Once your German bank account is sorted, the financial setup gets easier. Add health insurance, register your address, then start thinking about taxes and savings. Useful next reads:

- Live in Germany: finances pillar guide for the full money setup

- Cost of living calculator to size your monthly budget

- N26 bank account in Germany: deeper review if you want the full N26 walkthrough

- German bank account for international students for the student-specific path

- Expatrio services complete review if you also need a blocked account for your visa

Continue reading

Financial Planning·13 min read min read

ELSTER and German tax filing for expats: When you must file, how to claim back, what changed in 2026

Working in Germany and unsure about taxes? When ELSTER filing is mandatory, the 2026 changes, and how expats reclaim around 1,000 euro on average.

Read articleFinancial Planning·13 min read min read

Blocked Account Germany 2026: How much you need, providers compared, application steps

How much money you need in a 2026 German Sperrkonto, which providers are still operational, and the step-by-step application timeline before your visa appointment.

Read articleFinancial Planning·12 min read min read

€50,000 salary in Germany: Where it goes the furthest (Munich vs Berlin vs Leipzig)

A €50,000 salary in Germany is roughly €2,695 net per month. See exactly what that buys in Munich, Berlin, and Leipzig in 2026.

Read articleReady to plan your Germany journey?

Explore our tools and resources to find the perfect university and program for your academic goals.