Schufa in Germany explained: How to build credit as a new arrival, and the myths to ignore

Schufa is Germany's main credit file. Here is how it actually starts, the new 2026 score model, and how to build it from zero as an expat.

Table of contents

Last updated: May 2026

TL;DR: Schufa is Germany's main credit file. You start with no record on day one and you cannot import a foreign credit history. Register your address, open a German bank account, pay every direct debit on time for six to twelve months, and your file builds itself. The free GDPR data copy at meineschufa.de tells you what is on file. The €29.95 Bonitätsauskunft is the version landlords actually accept.

Schufa is the single most asked-about piece of German bureaucracy among new arrivals, and most of what gets repeated in expat groups is half right. The score itself is not your "permission to rent". The free data copy is not the document a landlord wants. Your home country credit history does not carry over. And as of January 2026, Schufa runs on a new 12-criteria model that replaced the old 250-point algorithm, which changes what actually moves your score.

This guide walks through what Schufa is, how a record starts when you arrive, what the new 2026 score measures, how to get your report (the free way and the paid way), how to build your score from zero inside your first year, and the persistent myths to ignore. If you are still figuring out the surrounding pieces, the Live in Germany pillar lays out the full bureaucracy stack and our finances guide for international students covers the practical money side.

What Schufa is in one paragraph

Schufa Holding AG is Germany's largest credit bureau, founded in 1927, with about 70 million consumer records. It collects payment behaviour data from banks, telecom providers, energy utilities, mobile phone carriers, mail-order retailers, and landlords who choose to report. It does not collect your salary, your tax data, your nationality, your employer, your religion, or your political views. It outputs a score that lenders and landlords use to decide whether to extend credit or sign a tenancy contract with you. Every adult registered in Germany ends up with a Schufa file the moment they open their first contractual relationship with a reporting partner, which for most new arrivals means their first German bank account or their first phone contract.

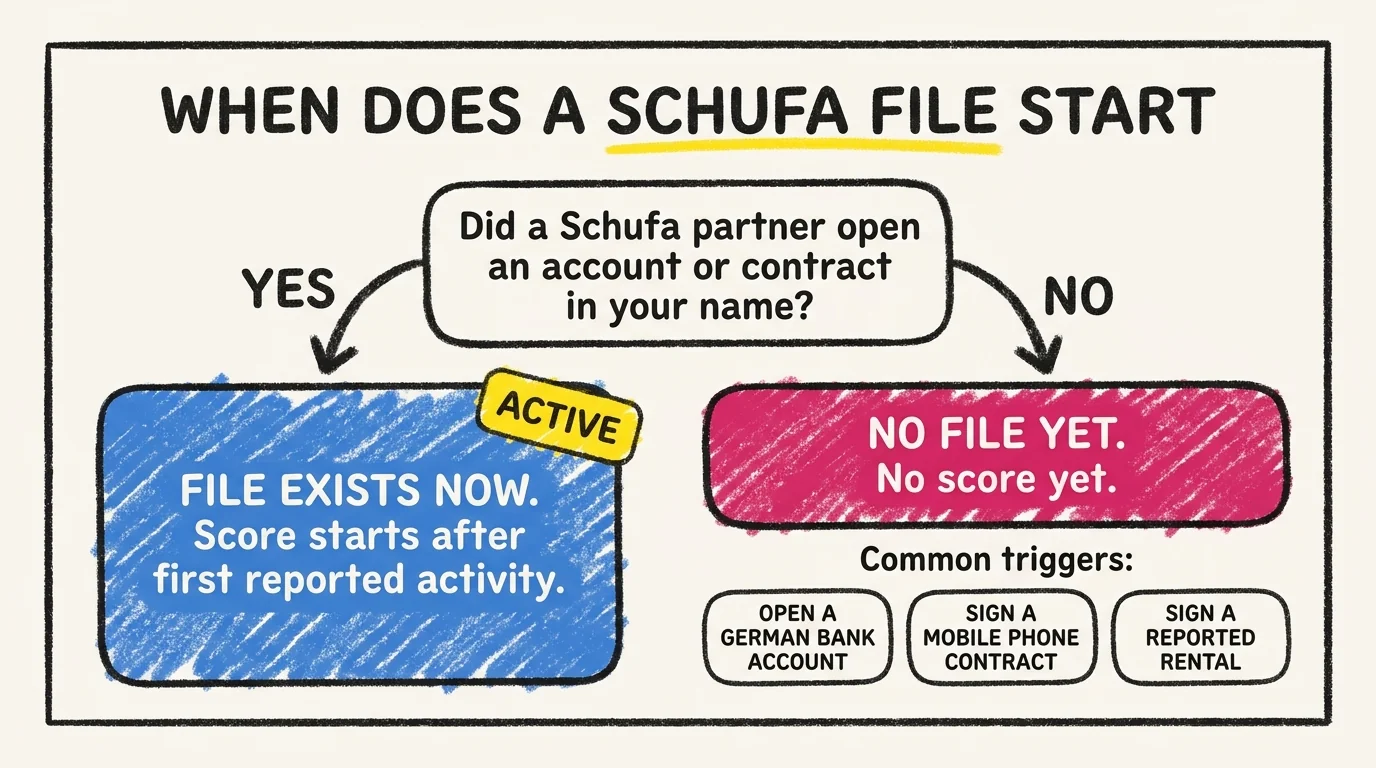

How Schufa actually starts when you arrive in Germany

Your Schufa file does not exist on landing day. It is not created by Anmeldung, by a visa, or by a residence permit. It is created the first time a Schufa-reporting company opens an account or contract in your name and reports the relationship to Schufa. For 95% of new arrivals, the trigger is one of three things: opening a German current account, signing a mobile phone contract, or activating a financed item like a bicycle on installments.

This matters because the timeline most expat forums quote ("you get a Schufa six months after Anmeldung") is wrong. Anmeldung registers you with the city. It does not register you with Schufa. The two systems are unrelated. A new arrival who lands, registers, and walks straight into a German bank account on week one will have a Schufa file by week two. A new arrival who keeps using their home country card for the first three months and signs no German contract will have no Schufa file at the three-month mark.

What absolutely does not transfer: your CIBIL score from India, your FICO from the US, your CRIF in Italy, your Equifax in the UK. Schufa has no formal data-sharing agreement with foreign credit bureaus. Your past does not count, your future starts at zero. This is annoying when applying for your first German apartment but it is also why a clean foreign track record cannot help you and a messy foreign track record cannot hurt you.

How the new 2026 Schufa score works

In January 2026, Schufa rolled out a new scoring model that replaced the legacy "branch-specific" score. The legacy model used roughly 250 unspecified data points behind a black box and produced a percentage score (the famous "97.3%"). The new model uses exactly 12 transparent criteria and produces a score on a 0 to 9,999 scale, with bands at 0 to 1,000 (very high risk), 1,001 to 5,000 (high risk), 5,001 to 8,500 (medium), 8,501 to 9,500 (low), and 9,501 to 9,999 (very low risk). Most German residents sit in the 9,000s. Anything above 9,700 reads as "very low risk" to lenders and landlords.

The 12 criteria, in plain English, are: how long your oldest credit relationship has existed; how long your current address has been on file; the number of active credit accounts you currently hold; the average age of those accounts; whether you have any reported payment defaults in the last 36 months; whether any defaults are still unsettled; whether any insolvency proceedings are open; the total number of credit applications in the last 12 months; the share of your credit lines you are actually using; whether your most recent payment activity is regular; the diversity of your credit relationships; and a residual model adjustment for behavioural patterns. Schufa publishes the full criteria list at schufa.de/en/score.

What changed in practice: address-of-record now matters more, frequent moves now matter more, the number of credit-check inquiries now matters less per inquiry but more in aggregate, and the share of your credit limit you actually use is now a top-five factor. For a new arrival the takeaway is simple. You start with a thin file. The system needs about six months of regular activity to produce a reliable score. Anything sooner is provisional.

How to get your Schufa report

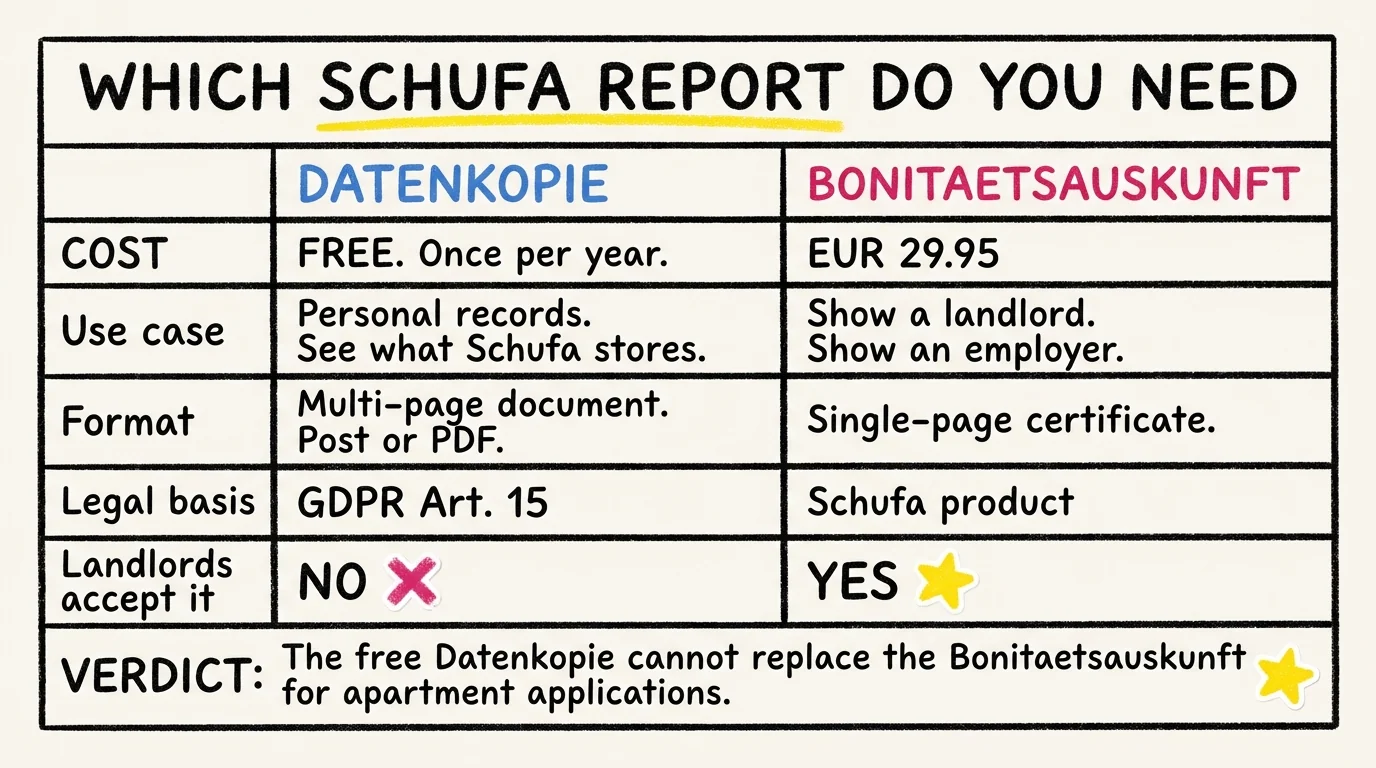

There are two reports and they are not interchangeable. New arrivals confuse them constantly and end up paying for the wrong one or sending the wrong one to a landlord.

| Report | Cost | Use case | Format | When you actually need it |

|---|---|---|---|---|

| Datenkopie nach Art. 15 DSGVO | Free, once per year | Your own records, see what Schufa stores about you | Multi-page document, by post or PDF, marked "Datenkopie" | Whenever you want to audit your file or dispute something |

| Bonitätsauskunft | €29.95 | Show a landlord, an employer, or a leasing company | Single-page certificate, freshly dated, marked "Bonitätsauskunft" | Apartment applications, car leasing, some sublet contracts |

The free Datenkopie is your right under EU law (GDPR Article 15). Order it at meineschufa.de under "Datenkopie nach Art. 15 DSGVO". Schufa is required to send it free of charge once per calendar year. It arrives by post in roughly 10 to 14 days, or as a PDF download if you complete identity verification online. It looks like an internal record sheet. Landlords typically reject it because it is not the format the German rental market expects.

The Bonitätsauskunft is the certificate landlords actually want. Order it at meineschufa.de or through ImmoScout24 (€29.95). It is a single page with your name, your current address, your overall risk verdict, and the issue date. Most landlords want a Bonitätsauskunft no older than three months. If you are doing a heavy apartment search, plan on one Bonitätsauskunft per major round, not per application. Landlords accept the same recent certificate from multiple applicants.

A few practical traps to avoid. Some third-party sites sell what looks like a free Schufa report and charge you a recurring monthly subscription for "Schufa monitoring". Schufa itself does not run those. Schufa direct, ImmoScout24, and a small number of bank partner integrations are the legitimate channels. If a service charges more than €30 for a single Bonitätsauskunft, you are paying a markup.

How to build your score from zero in your first year

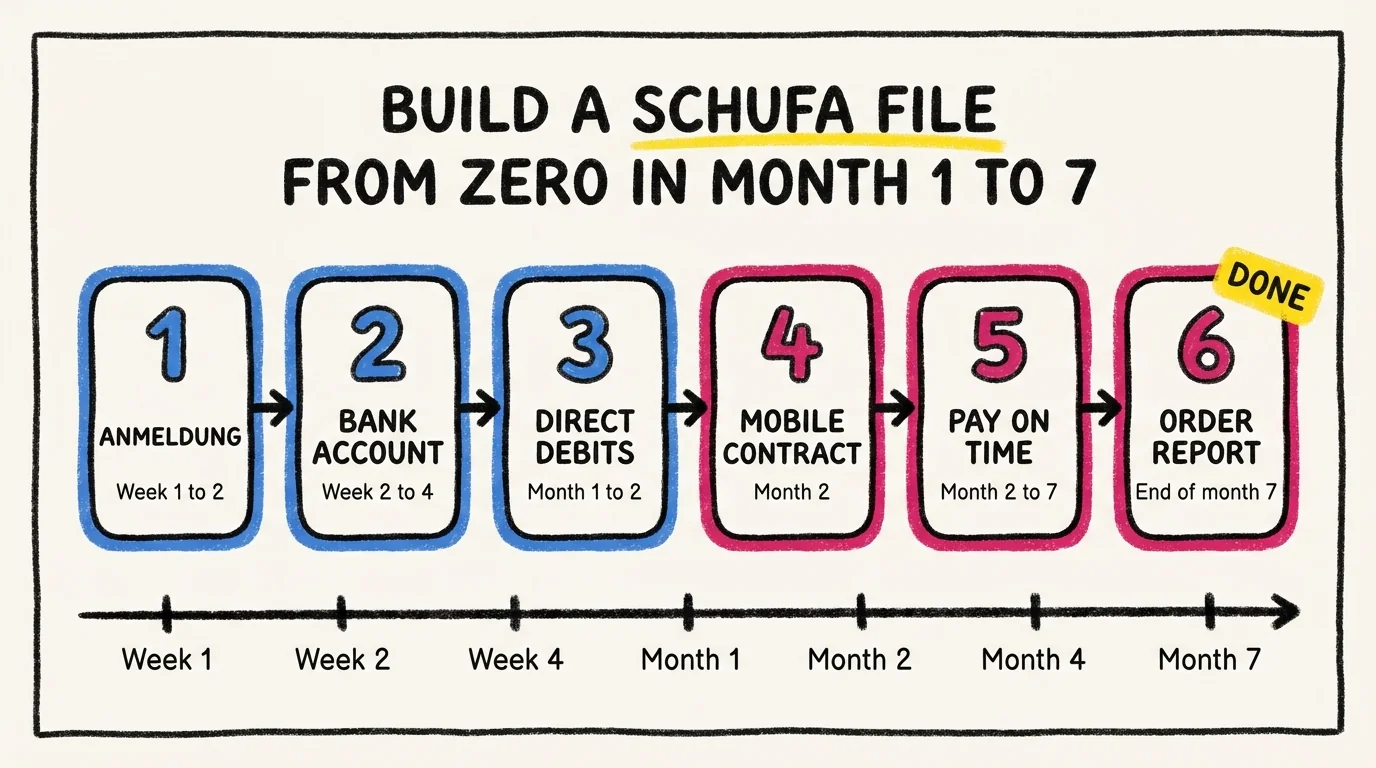

You cannot speed-run a Schufa score. You can speed-run the conditions that let it start being calculated. The order of operations below is what works for the median new arrival, with no special connections and no German guarantor.

Step 1, weeks 1 to 2: complete Anmeldung at the Bürgeramt. This does not create a Schufa file but every later step asks for the registration confirmation. Without it, no German bank will open a current account.

Step 2, weeks 2 to 4: open a German current account at any provider that reports to Schufa. Most major banks do, including Sparkasse, Commerzbank, Postbank, ING, DKB, Comdirect, and N26. The act of opening the account creates your Schufa file. Funding the account is not what triggers it; the contract relationship is. Our German bank account guide walks through which providers open accounts for new arrivals without a six-month German history requirement, and the N26 deep dive covers the most popular smartphone-first option.

Step 3, month 1 to 2: set up at least two recurring direct debits (Lastschriften) from this account. Health insurance, mobile phone, gym, Netflix, Deutschlandticket, electricity. The point is regular outflows that report payment behaviour. A current account with no activity does not move your score.

Step 4, month 2: sign a German mobile phone contract on a 24-month postpaid plan rather than a prepaid SIM. Postpaid contracts report to Schufa, prepaid does not. If a postpaid contract is rejected because you have no score yet, ask for a SIM-only deal or a contract with a smaller monthly amount; rejection itself is not reported negatively as long as the contract is never opened.

Step 5, months 2 to 7: pay every direct debit on time, every month, with no bounces. A single bounced direct debit (Rücklastschrift) for insufficient funds will not torch your file but it does get noticed in the new 12-criteria model under "regular payment activity". Two or three in six months will block you out of most apartment shortlists.

Step 6, end of month 7: order a Bonitätsauskunft. This is the first point where your score is statistically meaningful. Anything you order before month six will say something close to "insufficient data" and is useless for an apartment application.

What this gets you in numbers: a clean file at month 7 typically scores in the 9,200 to 9,500 band. That is enough for most private landlords in Berlin, Frankfurt, Munich, and Hamburg, especially if you also show three months of bank statements and proof of income. If you arrive with a blocked account and use that as your funding source for the first six months, the blocked account itself does not create a Schufa entry, but the German current account you set up to receive monthly disbursements does.

The myths to ignore

A short list of beliefs that get repeated in expat groups but do not hold up.

Myth: "Anmeldung creates your Schufa." False. Anmeldung registers you with the city for tax and residence purposes. It is not reported to Schufa. The two systems are unrelated.

Myth: "Your home credit score transfers." False. Schufa does not import data from CIBIL, FICO, Equifax, CRIF, or any other foreign bureau. The wall is total.

Myth: "Checking your own Schufa lowers it." False. Self-checks are flagged differently from lender inquiries and do not affect your score. Bank-initiated inquiries are also flagged as "Anfrage Kreditkonditionen" and do not lower your score; only the harder "Anfrage Kreditbewilligung" does.

Myth: "A high savings balance helps your score." False. Schufa does not see your account balance. It only sees the existence of the account and your direct debit return rate. A €50,000 balance and a €500 balance produce the same Schufa score, all else equal.

Myth: "Closing a credit card improves your score." Usually false. Under the new 12-criteria model, the average age of your accounts is a top-five factor. Closing your oldest account shortens that average and can drop your score in the short term. Keep old accounts open at zero balance unless they have annual fees you are unwilling to pay.

Myth: "You need a German guarantor for a Schufa." False. A guarantor (Bürge) helps with apartment applications when you have a thin file. It does not create a Schufa entry for you and you do not need one to open a German bank account.

Myth: "All apartment listings require a Bonitätsauskunft." Mostly false at the lower end of the market. Studierendenwerk dorms, WG-Gesucht room shares, and informal sublets typically do not. Private landlords on ImmoScout24 in tier-1 cities almost always do.

What hurts your score (and what does not)

Things that hurt: late or returned direct debits; unpaid mobile phone bills sent to collections; opening many credit accounts in a short window; defaulting on a Sparkasse overdraft (Dispositionskredit); insolvency proceedings; identity-theft entries you have not disputed.

Things that do not hurt: applying for a residence permit; registering at a new address (one move per year is normal); checking your own Schufa file; bank-initiated rate inquiries; closing one of several active accounts when others remain open at least a year; paying off a loan early.

If you find a wrong entry on your Datenkopie, dispute it in writing to Schufa with documentation. Schufa is required to investigate within 30 days under GDPR. If they do not remove a verified-wrong entry, the next step is the Bundesdatenschutzbeauftragter (federal data protection commissioner), which is free and reasonably effective.

FAQ

How long does a negative Schufa entry stay on file?

Three years from the date the debt is fully settled. An unsettled debt stays indefinitely. A paid-off mobile phone bill that went to collections in May 2026 will fall off your file in May 2029 if you settled it on the same date.

Can I get a Schufa as a non-resident before I arrive?

Practically, no. The free Datenkopie can only be sent to a German address. The €29.95 Bonitätsauskunft requires identity verification through a German bank or PostIdent. New arrivals should plan to start the file in week 2 to 4 after Anmeldung, not before arrival.

Do EU citizens have a different Schufa process from non-EU citizens?

No. Schufa does not record nationality. The process is identical for an Indian arrival on a Blue Card and a French arrival on freedom of movement. Both start at zero, both build the file the same way.

Will my Schufa score follow me if I move within Germany?

Yes. Your file is tied to your name and date of birth, not your address. Address changes are recorded but the score is portable across the country. Multiple addresses in 12 months can dent the "address stability" factor under the new model.

Can a landlord reject me for having no Schufa rather than a bad Schufa?

Yes, and they often do. A "no file" reading reads to landlords as "unknown risk" rather than "low risk". The fix is offering compensating evidence: three months of bank statements, employer offer letter, blocked account confirmation, parental Bürgschaft, or a higher deposit (the legal max is three cold-rent months, German law caps it).

What is the cheapest legitimate way to get a Bonitätsauskunft?

Schufa direct at meineschufa.de for €29.95 is the floor. ImmoScout24 premium members get a small discount. Anything cheaper is either the free Datenkopie sold under a confusing name, or a recurring subscription pretending to be a one-off. Avoid both.

How do I dispute a wrong Schufa entry?

Send a written dispute to Schufa Holding AG, Postfach 10 25 66, 44725 Bochum, with copies of evidence (proof of payment, contract terminations). Reference Article 16 GDPR. Schufa must respond within 30 days. Keep proof of postage. If the dispute is rejected and you have documentation, escalate to the federal data protection commissioner.

Does freelancing affect my Schufa score?

Not directly. Schufa does not see your income source or amount. It sees the regularity of your direct debits and the absence of returned payments. Freelancers with steady direct-debit history score the same as salaried employees with steady direct-debit history, all else equal. The trick is funding your account in time for monthly outflows even when client payments are lumpy.

Where to next

- The pillar route on Schufa and your German credit file covers what comes after the report stage, including dispute templates and rental application packets.

- For the bank-account side of building your file, our guide on opening a German bank account lists every provider that opens accounts for new arrivals without a six-month residency requirement.

- For 2026 monthly fees, free-ATM networks, English support, and Anmeldung rules across the major German banks, see the best German bank accounts for expats in 2026 comparison.

- For the everyday-money side, the practical finance guide for international students covers Lastschriften, standing orders, and how to keep your direct debits clean during your first year.

- If you arrived on a blocked account, the blocked account activation walkthrough shows how the monthly disbursement gets routed to your German current account, which is the actual Schufa-reporting relationship.

Continue reading

Living in Germany·19 min read min read

Public vs Private Health Insurance in Germany: PKV vs GKV Head-to-Head with Real Numbers

Public vs private health insurance in Germany compared with 2026 numbers. JAEG, BBG, GKV monthly cost, PKV premiums, family math, and the age 55 lock-in.

Read articleLiving in Germany·15 min read min read

Rundfunkbeitrag explained: why every German household pays it and how students legally skip it

Germany's broadcasting fee in 2026: who pays, who is exempt, how to apply for the Befreiung, and what happens if you ignore the bill.

Read articleLiving in Germany·16 min read min read

Anmeldung in Germany 2026: How to actually get a Bürgeramt appointment in Berlin, Munich, Hamburg

Anmeldung in Germany 2026: how to actually get a Bürgeramt appointment in Berlin, Munich and Hamburg. Wait times, documents, fines, online route.

Read articleReady to plan your Germany journey?

Explore our tools and resources to find the perfect university and program for your academic goals.